.jpg)

.jpg)

.jpg)

Home Loan vs Mortgage Loan Explained Simply

If you’ve ever asked, “Is a home loan the same thing as a mortgage loan?”, you’re not alone. The two terms are often used interchangeably in the U.S., but they don’t always mean the exact same thing.

This guide explains the difference in plain English, shows when it actually matters, and helps you communicate clearly with lenders, real estate agents, and your closing team.

The simplest definition (most people need)

In everyday conversation:

- Mortgage loan usually means the loan you use to buy a home (or refinance the one you already own).

- Home loan is often used as a casual synonym for “mortgage.”

So if you’re shopping for a 30-year fixed to buy a primary residence, most people will understand “home loan” and “mortgage loan” the same way.

Where it gets confusing is that “home loan” can also be a broader umbrella term that includes other types of home-related financing, like tapping equity.

What “mortgage” actually is (the legal piece)

A mortgage is not the money itself. It’s the legal agreement (lien) that secures a loan with real estate.

In other words:

- The loan is the money you borrow.

- The mortgage (or deed of trust in many states) is the instrument that gives the lender a claim against the property if the loan isn’t repaid.

If you want an official definition, the Consumer Financial Protection Bureau’s mortgage glossary is a reliable reference.

Mortgage vs deed of trust (quick note)

Depending on your state, the security instrument may be called a mortgage or a deed of trust. Borrowers still commonly say “mortgage payment” either way. Functionally, both secure the loan with your home.

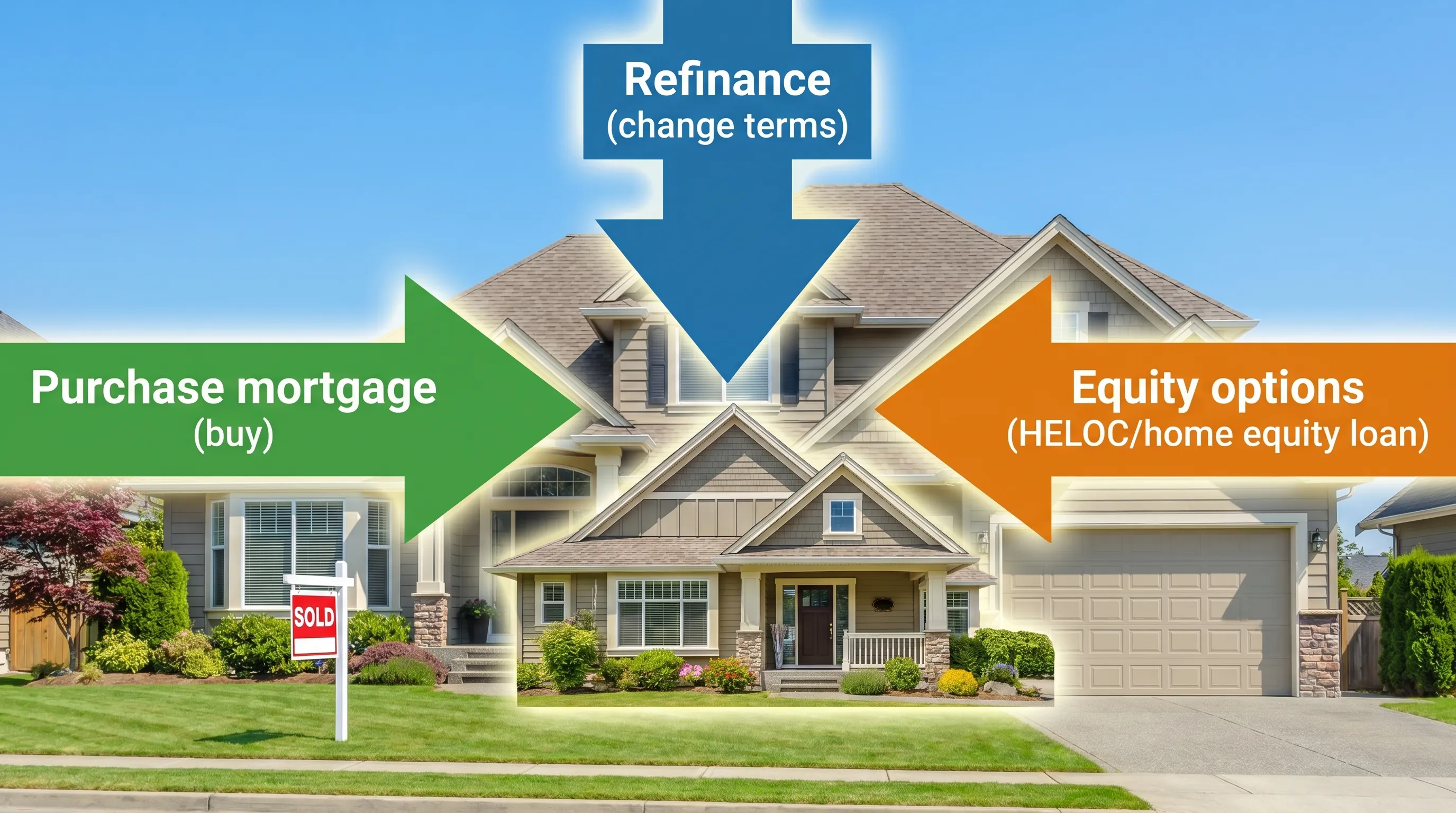

What “home loan” can mean (the broader category)

Home loan is a more flexible phrase. It can refer to any loan connected to a home, including:

- Purchase mortgage (buying a home)

- Rate-and-term refinance (changing rate and/or term)

- Cash-out refinance (refinancing and taking cash from equity)

- Home equity loan (second mortgage, usually a lump sum)

- HELOC (home equity line of credit, a revolving line)

- Construction or renovation loans (specialized programs)

So, all mortgage loans are “home loans” in a general sense, but not every home loan is what people mean by “a mortgage” for buying a house.

Home loan vs mortgage loan: When the difference matters

Most of the time, the difference is semantic. But there are a few moments when using the right term can prevent miscommunication.

1) When you’re tapping equity, not buying

If you say, “I want a home loan,” a lender may ask a follow-up: “Purchase or equity?”

Examples:

- You own your home and want $40,000 for renovations.

- You might be looking for a HELOC, a home equity loan, or a cash-out refinance.

- You’re buying a new home.

- You likely mean a purchase mortgage.

These are very different products with different rates, costs, and timelines.

2) When there are two loans on the property

You can have more than one mortgage loan at once.

- First mortgage: the primary loan used to buy the home (or the main refinance).

- Second mortgage: an additional loan (like a home equity loan or HELOC) that sits behind the first.

In that case, saying “mortgage loan” without specifying first or second can create confusion.

3) When you’re comparing offers and fees

People sometimes assume a “mortgage loan” is one standard product. In reality, the loan type and structure change everything.

Two borrowers can both say “I’m getting a mortgage,” but one might be getting:

- A 30-year fixed conventional loan with PMI

- An FHA loan with mortgage insurance premiums

- A VA loan (for eligible borrowers) with no monthly PMI

- A 5/6 ARM with a lower initial rate

If you want apples-to-apples comparisons, the word choice is less important than the details on your Loan Estimate (rate, APR, fees, cash to close, and monthly payment).

The real question to ask: “What kind of home financing do I need?”

Instead of focusing on the label, clarify your goal. Most borrowers fall into one of three buckets.

Bucket A: Buying a home (purchase mortgage)

This is what most people mean by “mortgage loan.” You borrow money to purchase a property and repay it over time.

Key decisions include:

- Loan program (conventional, FHA, VA, USDA, jumbo, etc.)

- Down payment strategy

- Rate structure (fixed vs ARM)

- Term (often 30 years, sometimes 15 or 20)

Bucket B: Replacing your current mortgage (refinance)

A refinance swaps your existing mortgage for a new one. Common goals:

- Lower the interest rate (or APR)

- Reduce monthly payment

- Shorten the term

- Move from an ARM to a fixed rate (or vice versa)

- Remove mortgage insurance (when eligible)

Bucket C: Using your equity (home equity loan, HELOC, or cash-out refi)

Equity-focused borrowing can be powerful, but it’s also where terminology gets messy.

- HELOC: flexible, revolving line, often variable rate.

- Home equity loan: usually a lump sum, often fixed rate.

- Cash-out refinance: replaces your existing mortgage with a bigger one and gives you the difference in cash.

Each has tradeoffs in rate, closing costs, and payment stability.

A plain-English cheat sheet (quick comparisons)

Here’s a simple way to translate common phrases you’ll hear:

- “Home loan”: could mean any home-related financing.

- “Mortgage loan”: usually a first mortgage used for purchase or refinance.

- “Second mortgage”: a home equity loan or HELOC that sits behind your first mortgage.

- “Lien”: the lender’s legal claim on the property as collateral.

- “Mortgage payment”: your monthly principal and interest (often plus escrow for taxes and insurance).

What to focus on instead of the wording

Whether it’s called a home loan or mortgage loan, these are the numbers and rules that actually determine what the financing feels like.

Interest rate vs APR

The interest rate impacts your payment. The APR includes certain fees and costs to help you compare offers more fully.

APR is useful, but it isn’t perfect. For example, it may not fully capture how long you’ll keep the loan or what you’ll do with the property later.

Total monthly housing payment (not just principal and interest)

Your true monthly cost often includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- Mortgage insurance (if required)

- HOA dues (if applicable)

Cash to close

Borrowers often get surprised by cash-to-close because they focus only on down payment. Your total cash needed can also include lender fees, third-party fees, prepaids, and escrows.

Occupancy and property type

Many loan options depend on whether it’s:

- Primary residence

- Second home

- Investment property

And on what you’re buying (single-family, condo, 2–4 unit, manufactured, etc.).

A practical tip: organize your money trail early

One reason mortgage processes feel stressful is that your lender is verifying a lot of financial information in a short time.

Two simple habits help:

- Keep your income, bank activity, and large transfers easy to explain.

- If you run a small business, keep your business payments and reconciliation clean so bank statements tell a clear story.

For example, travel agencies and travel businesses sometimes use a centralized payment platform like Elia Pay to simplify reconciliation and reduce fraud risk, which can make financial records easier to manage when applying for any major credit.

What to ask a lender so you get the right “home loan”

If you want to cut through jargon quickly, ask questions that force clarity:

- Is this a purchase, refinance, or equity loan scenario?

- Is this a first mortgage or second mortgage?

- What loan programs am I eligible for based on credit, income, and down payment?

- What is the rate, the APR, and the total estimated cash to close?

- Is the rate fixed or adjustable? If adjustable, what can the payment become later?

- What documentation is most likely to slow underwriting in my situation?

A good lender will answer in plain language and provide side-by-side scenarios when it helps.

Where New Era Lending fits in

If you’re trying to translate terminology into a real decision, the most helpful step is usually not learning more definitions. It’s getting a clear comparison based on your numbers.

New Era Lending helps borrowers across 39 states with home purchase, refinancing, and equity access by combining:

- Smart technology tools (secure document uploads, e-signature support)

- Personalized human guidance from mortgage professionals

- A focus on transparent rates and terms and a streamlined path to approval

That mix is especially useful when you’re not sure whether you need a “mortgage loan” in the strict sense (purchase or refinance) or a broader “home loan” solution that uses your equity.

Frequently Asked Questions

Is a home loan the same as a mortgage loan? Most of the time, yes, people use them interchangeably. Technically, “home loan” can be broader and include equity loans like HELOCs and home equity loans.

Why do some people say “mortgage” if they mean the loan? In everyday U.S. usage, “mortgage” often refers to the loan and the security instrument together. Legally, the mortgage is the lien that secures the loan.

What is the difference between a mortgage and a deed of trust? They’re both ways to secure a home loan with the property. Different states commonly use one term or the other, but borrowers still typically call the payment a mortgage payment.

Is a HELOC a mortgage loan? A HELOC is usually considered a type of home loan and can be a form of second mortgage because it’s secured by your home, but it’s not the same as a standard purchase mortgage.

How do I know if I should refinance or take a home equity loan? Refinancing replaces your current mortgage (and can change your rate and term). A home equity loan or HELOC adds another loan on top of your existing mortgage. The best choice depends on your current rate, your cash need, and the total cost.

What matters more than the term “home loan” or “mortgage loan”? The details: loan purpose (buy/refi/equity), program type, rate structure, APR and fees, cash to close, and how the payment fits your budget.

Ready to compare your options with real numbers?

If you’re deciding between a purchase mortgage, refinance, or an equity-based home loan, New Era Lending can walk you through clear scenarios so you can choose confidently. Visit New Era Lending to explore options and start a personalized conversation.