.jpg)

.jpg)

.jpg)

Equity Home Loans: How Much Can You Borrow and at What Cost?

Tapping into your home’s equity can be a smart way to fund big goals, but “How much can I borrow?” is only half the question. The other half is “What will it really cost me, month to month and over time?” Equity home loans can look similar on the surface, yet borrowing limits, rates, fees, and risk can vary a lot depending on the product and your financial profile.

Below is a practical way to estimate your borrowing power and understand the true cost, so you can compare options confidently.

What counts as an equity home loan?

In everyday conversation, “equity home loans” often includes three common ways to access equity:

- Home equity loan: A lump sum with a fixed rate and fixed monthly payment (like a second mortgage).

- HELOC (home equity line of credit): A revolving credit line you can draw from as needed, usually with a variable rate.

- Cash-out refinance: You replace your current mortgage with a larger one and take the difference in cash.

If you want a deeper comparison of the first two, New Era Lending breaks it down clearly in Equity Mortgage Loan vs HELOC: Which Is Better for You?

How much can you borrow with equity home loans?

Your maximum borrowing amount is mostly determined by three things:

- Your home’s market value (typically supported by an appraisal or automated valuation model)

- How much you still owe on any mortgages

- The lender’s maximum LTV/CLTV limit

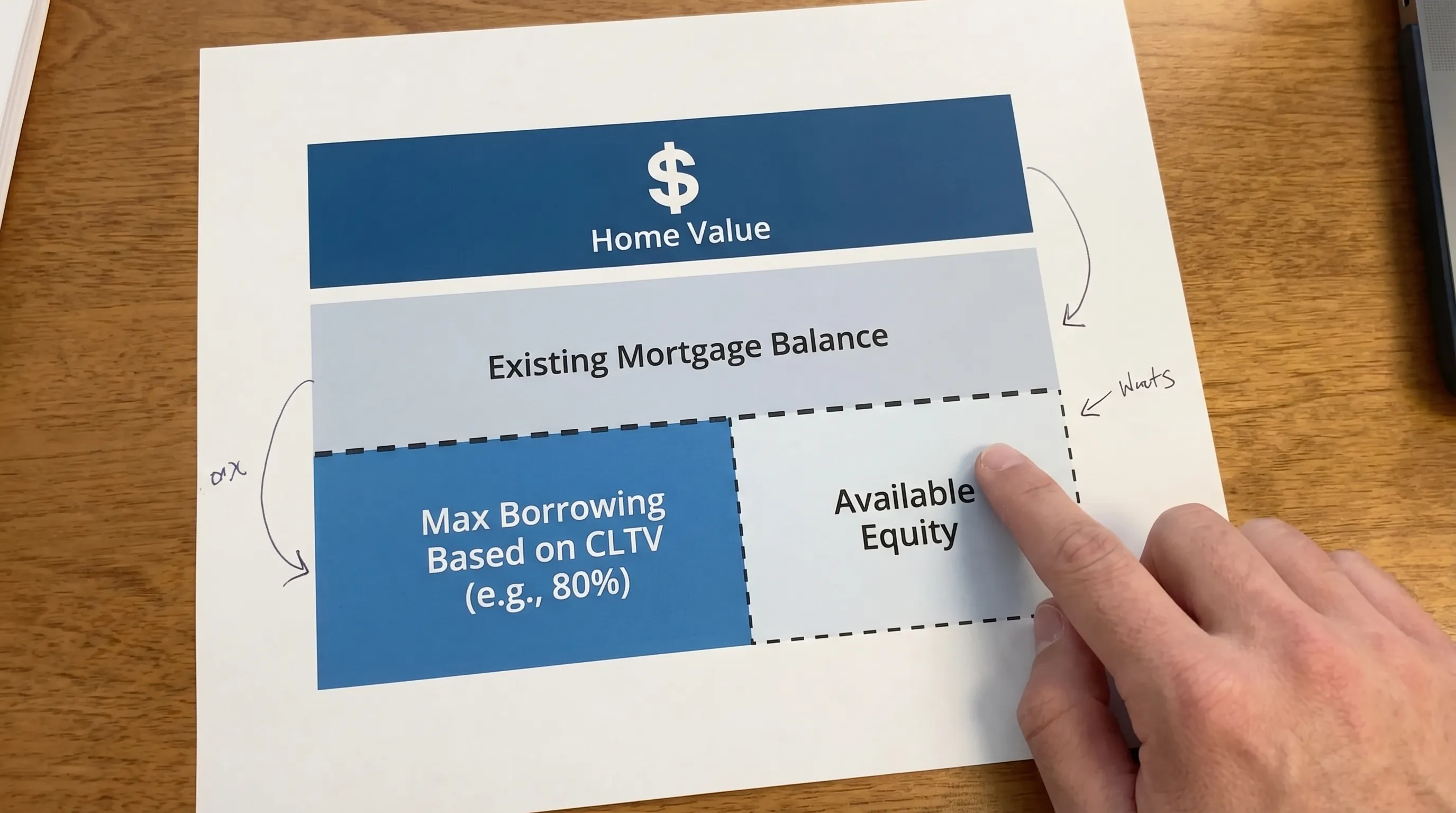

The key formula: CLTV (combined loan-to-value)

For equity products, lenders usually focus on CLTV, which accounts for all loans secured by the home.

CLTV = (current mortgage balance + new equity loan/HELOC limit) ÷ home value

Many lenders cap CLTV around 80% to 85%, and some scenarios may go higher (often up to 90%) for strong credit and certain property/occupancy types. The exact cap depends on the lender, your profile, and whether it’s a primary residence, second home, or investment property.

A quick borrowing estimate (with real numbers)

Let’s say:

- Home value: $500,000

- Current mortgage balance: $320,000

- Target max CLTV: 85%

Step 1: Calculate the max total debt allowed at 85% CLTV.

- 0.85 × $500,000 = $425,000

Step 2: Subtract what you already owe.

- $425,000 − $320,000 = $105,000

In this simplified example, $105,000 is a reasonable estimate of your maximum new borrowing (home equity loan amount or HELOC line limit), assuming you qualify.

Why your “max” may not be your approved amount

Even if the math says you have available equity, underwriting can reduce your limit because of:

- Debt-to-income (DTI) ratio: Your monthly debts relative to gross income

- Credit profile: Score, history, utilization, and recent inquiries

- Occupancy and property type: Primary residence is typically more flexible than rental

- Loan size and lien position: Second liens can price differently than first liens

- Documentation and income type: Self-employed or variable income can require more analysis

If your income is complex, it helps to understand how lenders view it. New Era Lending covers the documentation and qualification side in How to Qualify For a Self-Employed Mortgage Loan.

What does an equity home loan cost?

Cost is more than the interest rate you see in an ad. To compare options cleanly, look at:

- Interest rate (note whether it’s fixed or variable)

- APR (captures many fees and gives a more apples-to-apples comparison)

- Upfront closing costs (lender fees plus third-party fees)

- Ongoing costs (line fees, annual fees, and interest-only risk in a HELOC draw period)

- The opportunity cost of resetting your mortgage term (common with cash-out refinances)

Rates: why equity loans can price higher than first mortgages

A home equity loan or HELOC is often a second lien behind your primary mortgage. Second liens can carry more risk for lenders, so rates may be higher than first-mortgage rates, even for well-qualified borrowers.

HELOCs are frequently variable-rate, commonly tied to an index such as the prime rate, plus a margin. That means your payment can rise even if your balance does not.

Cash-out refinances are first liens, but because you’re increasing the loan amount and pulling cash out, pricing can be different from a standard rate-and-term refinance.

For consumers comparing loan costs, the Consumer Financial Protection Bureau has a helpful explainer on how to read a Loan Estimate and where fees show up.

Fees and closing costs: what to expect

Exact fees vary by lender and state, but many equity transactions involve some mix of:

- Appraisal or valuation fee

- Credit report fee

- Origination or underwriting fees (sometimes called lender fees)

- Title search and title insurance (varies by lien position and state)

- Recording and settlement fees

Some HELOCs advertise “low to no closing costs,” but it’s important to read the fine print. A lender might cover certain fees upfront, then recoup costs via a higher rate, an annual fee, or an early closure fee.

The monthly payment: fixed vs variable matters more than people think

A fixed-rate home equity loan is predictable. A HELOC can be flexible, but payments can change because:

- Your balance changes as you draw and repay

- Your interest rate changes if it is variable

- Some HELOCs start with interest-only payments during the draw period, then shift to principal and interest, which can increase required payments significantly

When you compare offers, ask for a “stress test” payment example, such as what the payment would be if rates rise by 1% to 2%.

The hidden cost most borrowers miss: how long you’ll carry the debt

Two borrowers can take the same $100,000 from their equity and pay very different total costs depending on payoff strategy.

- If you use a HELOC as a long-term loan and only pay the minimum, total interest can balloon.

- If you do a cash-out refinance and restart a 30-year term, you may reduce the monthly payment while increasing lifetime interest paid.

That does not mean these options are “bad.” It means you should match the product to your goal and timeline.

A practical rule: match the product to the project

- One-time expense with a clear budget (roof, consolidation payoff, major remodel): a fixed-rate home equity loan can be easier to manage.

- Multi-stage expense with uncertainty (renovation in phases, ongoing tuition, emergency liquidity): a HELOC’s flexibility can help, if you can handle variable-rate risk.

- Large cash need with a strong reason to replace your current mortgage anyway: a cash-out refinance can make sense, especially if it improves your overall structure, not just the cash in hand.

Tax considerations (important, but easy to misunderstand)

Interest on home equity borrowing is not automatically deductible. Under current IRS rules, the interest deduction is generally limited to situations where the funds are used to buy, build, or substantially improve the home that secures the loan, and limits can apply. Because tax situations vary, it’s wise to review the IRS guidance and confirm with a qualified tax professional.

You can start with the IRS overview on the home mortgage interest deduction.

What equity home loans are commonly used for (and when to be careful)

Homeowners use equity for many reasons, including:

- Home improvements that increase usability and potentially value

- Debt consolidation (especially high-interest credit cards)

- Major life events (education costs, medical expenses, family support)

- Building a cash buffer for self-employed income volatility

Some people also consider equity for discretionary spending, like weddings or extended travel. If you go that route, be honest about the risk: you’re converting lifestyle spending into debt secured by your home. If international travel is part of your plan, it can help to reduce friction and surprises on the logistics side too, for example with eVisa processing solutions that streamline border-crossing administration.

How to reduce the cost of borrowing against your equity

You cannot control every part of pricing, but you can improve the “inputs” lenders use.

Strengthen your equity position (even slightly)

- Make one or two extra principal payments on your first mortgage before applying, if timing allows.

- Consider whether a smaller loan amount keeps you under a better CLTV tier.

Improve your credit profile before you apply

- Pay down revolving balances (utilization can matter)

- Avoid opening multiple new accounts shortly before shopping

- Check your credit reports for errors

Shop using APR and total cost, not just rate

Two loans can have the same rate but different fees, or the reverse. Ask each lender for:

- A quote that includes rate, APR, estimated closing costs, and any ongoing fees

- Clear explanation of whether the rate is fixed, variable, or introductory

Be strategic about the structure

For HELOCs, ask about:

- Whether you can lock a portion into a fixed-rate segment (if offered)

- Draw period length and repayment period terms

- Margin, caps, and how often the rate adjusts

For home equity loans, ask about:

- Fixed term options (10, 15, 20 years)

- Whether there is a prepayment penalty

For cash-out refinances, make sure you understand:

- The new term length and how it changes total interest paid

- Whether you are giving up a very low existing first-mortgage rate

How New Era Lending can help you get accurate numbers (not guesses)

Online calculators are a good starting point, but equity decisions are usually “scenario problems,” not single-number problems. The best next step is to run side-by-side options that reflect your actual credit, income, property, and goals.

New Era Lending’s approach combines smart technology with personalized human guidance, so you can:

- Estimate borrowing limits based on realistic CLTV and qualification factors

- Compare product structures (home equity loan vs HELOC vs cash-out refi)

- Review rates and terms clearly, with attention to APR and closing costs

- Move through the process with secure document uploads and e-signature support

If you want to understand your realistic borrowing range and what it will cost at today’s pricing, request a personalized comparison through New Era Lending. A clear set of scenarios can turn “I think I can borrow…” into a confident, numbers-backed plan.